“The intrinsic value of these [container-ship leasing] companies can continue to move higher so long as the demand environment stays quite good. If it goes through the end of this year and into 2022, the intrinsic values of these companies are going to be significantly ahead of where they are today.” Amit Mehrotra, Deutche Bank

(CNW Group/Atlas Corp.)")

Atlas is a leading global asset manager that owns and operates the businesses in which it invests while focusing on deploying capital across multiple verticals. The current market capitalization is approximately $3.5bn with 246.8 million shares outstanding. I’ve been an investor in the company since it was simply Seaspan, which is now one of its subsidiaries.

Seaspan first came on my radar while digging through the holdings of Prem Watsa, often called the Canadian Warren Buffet. Through Fairfax Financial, he owns approximately 40% of the company (though he recently trimmed a small amount). Fairfax also is the majority owner of another company I’m also an investor - Eurobank Ergasias, which I plan to cover in a later post.

The company was formed in 1970 from a merger of Island Tug and Vancouver Tug, which dates back to the 19th century. It’s undergone a long series of mergers and acquisitions including an affiliation with the Washington Companies, founded by Dennis Washington. Washington, a self-made American billionaire who also owns a copper mine, a regional railroad, and stakes in two diamond mines became 100% owner of the company in 1996. He now owns 24% of the company at last filing in addition to Prem’s 40%.

Industry

Liner companies own a portion of their fleets and charter in the rest from non-operating owners (NOOs). U.S.-listed NOOs include Atlas Corp., Danaos (NYSE: DAC), Costamare (NYSE: CMRE), Global Ship Lease (NYSE: GSL), Navios Containers (NASDAQ: NMCI), Navios Partners (NYSE: NMM), Capital Product Partners (NASDAQ: CPLP) and Euroseas (NASDAQ: ESEA).

Building a large boat takes a long time and much like the housing industry there is currently a shortage of both containers and ships. Fearnleys estimates that the order book-to-fleet ratio needs to grow to 17% just to cover cargo demand through 2023. As of Thursday, March 25th, 2021, Asia-West Coast spot rates were at $4,292 per forty-foot equivalent unit (FEU), up 191% year-on-year. Asia-East Coast rates were $5,716 per FEU, up 109% year-on-year.

Marine transport remains the most fuel-efficient mode of global transportation, accounting for 90% of global transport, and demand has doubled between 2000 and 2019. Hellenic Shipping News recently printed the spot prices for container ships, and the trend is headed in a positive direction. Idle vessel counts are at historical lows with charter rates at near historical highs and the availability of any vessels about 4,000 TEU is very scarce.

The industry is undergoing a transition currently with the global push for decarbonization. Renewable powered ships are not yet economically viable, so the options are liquified natural gas or diesel. LNG produces 30% less carbon dioxide, but it costs more. New legally binding regulations, known as IMO 2020 kicked in on 1 January, requiring marine diesel to contain less than 0.5% sulfur. Shipping firms have three main choices: switch to expensive low sulfur fuel, fit "scrubbers" to remove the pollutants from exhaust gases - or use alternative fuels such as LNG. Atlas and most firms are going with scrubbers.

Business Model

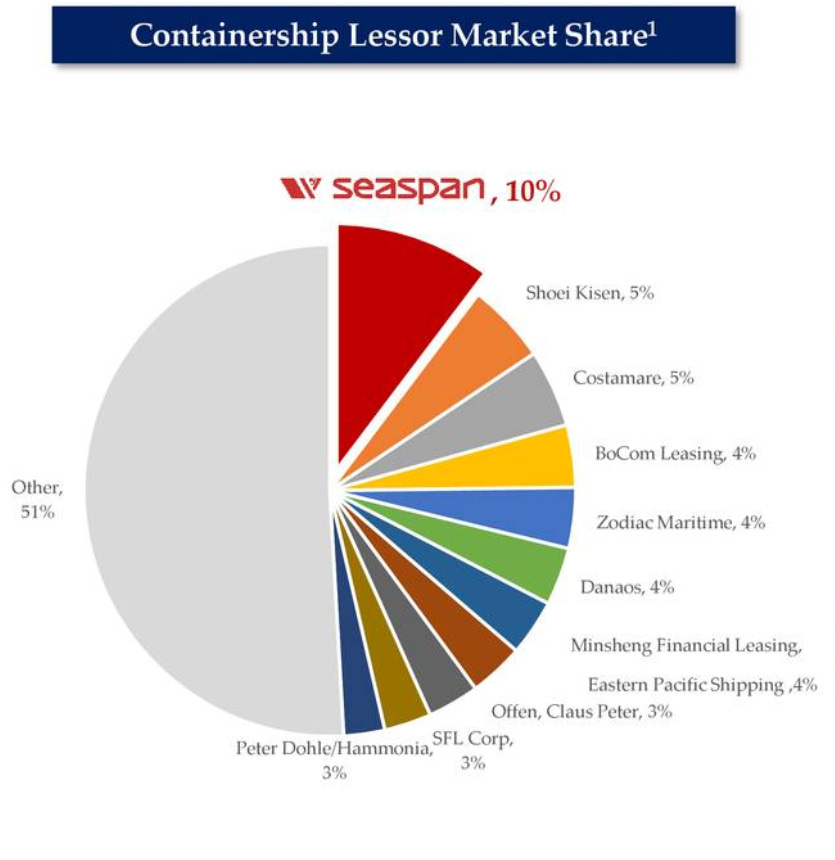

Atlas makes money through two divisions, Seaspan and APR Energy, its most recent acquisition. Seaspan accounts for ~86% of adjusted EBITDA. Seaspan has a fleet of 160 vessels, and offices in Hong Kong, Canada, and India making it the largest independent owner and operator of containerships in the world with around 10% of the global market share.

Seaspan has a relatively simple way to grow revenue, build or buy more ships and acquire leases for them. In addition to the 15 secondhand vessels acquired in 2020, the company has recently announced 31 new builds (all backed by long-term charter), a very aggressive pace.

Given this business's long-term nature, revenue is highly predictable as the company currently shows $10.7 billion in contracted cash flow. At 2020 year-end, more than 93% of Seaspan's 2021 revenue guidance at the midpoint is already contracted. Since 2017, Atlas has added 71 new vessels and over 890,000 TEUs, an 80% increase in a little over 3 years.

Gross margins have remained above 75% since 2011. Atlas does not appear to possess any competitive advantages outside of economies of scale and ample liquidity. This is evident as well by the fairly average return on invested capital, which has remained in the low single digits. Management is exceptional, with CEO Bing Chen a veteran of the last downturn in the industry. Mr. Chen is a Certified Public Accountant (inactive) and received a B.S., Accountancy (Magna Cum Laude) (Honors) from Bernard Baruch College, and an MBA (Honors) from Columbia Business School. Incoming CFO Graham Talbot, the newest member of the executive team has worked in asset-intensive industries, primarily in the energy sector, for more than 30 years. However, the name that turns most heads is Atlas Chairman, David Sokol.

In 2009 Buffet he described Sokol as an “enormously talented builder and operator.” Mr. Sokol has founded three companies to date, taken three companies public, and as Chairman and CEO of MidAmerican Energy Holdings Company, which he sold the Berkshire Hathaway, Inc. Sokol was widely thought of as a successor to Buffett (called Buffett’s Mr. Fix It, responsible for Berkshire investments in BYD among others). Sokol was given multiple CEO roles at Berkshire; under Sokol's leadership, Johns Manville was brought back on track and NetJets swung from a $157 million loss in 2009 to a $207 million gain in 2010. Sokol resigned after the Lubrizol acquisition in March 2011. At the time, Sokol was estimated to be worth over $100 million and earning $24 million in total compensation. It remains curious why he violated Berkshire company policy for what ultimately resulted in a $3 million profit (Sokol purchased Lubrizol stock before pitching the idea to Berkshire following a dinner meeting with the CEO) Sokol defended himself in a lengthy CNBC interview claiming he had no interest in the Berkshire CEO position, nor did he think that the Berkshire board would have an interest in the deal (which Warren admitted he initially declined) and it does seem to be more of a Berkshire corporate governance lapse than an attempt at insider trading. Berkshire’s loss, Atlas’ gain.

“If I think back at Mid American Energy, when we joined Berkshire in 2000, the company had about $10 billion in assets. Today, 21 years later, they're over $100 billion. And -- but that wasn't steady growth in each of the platforms, whether it was the pipeline platform, the U.S utility platform, the foreign utility platform or independent power, they all came in cycles and opportunistic cycles.” - David Sokol

APR Energy

APR Energy operates a similar cash flow model, currently with $300M in contracted cash flow giving the company a contracted gross of $11B. APR Energy operates the only mobile gas turbine fleet in the world with 9 powerplants currently in operation in 5 countries. Since the February 2020 acquisition, APR has been a laggard as operations ground to a halt due to declining energy demand from COVID. CEO Bing Chen spent some time assuring shareholders that the acquisition will prove timely in the coming years on the recent earnings call, though it seems ill-timed and thus far proven costly.

APR revenue grew from $308.3 million in 2013 to $485.7 million in 2014, the company’s fourth straight year of double-digit percentage growth. 2014 actually was a tough year for the company due to a massive $717.4 million write-off related to its operations in Libya, resulting in an operating loss of $702.5 million for 2014. Six years later the company is purchased for $750M. Atlas finalized its purchase price allocation for the APR acquisition in Q4 2020. The company recently wrote off $117.9 million of goodwill, which they attributed to lack of demand due to the pandemic.

Recently released APR revenue guidance at $180M to $205M, with debt at the division of $228M. APR will need to outperform to justify this acquisition going forward. On the earnings call, Sokol indicated that APR will be seeking an ISO 4001 Environmental Management System certification for 2021.

As of December 31, 2020, Atlas had total liquidity of $771.3 million, consisting of $304.3 million of cash and cash equivalents and $467.0 million of availability under undrawn committed credit facilities. As of December 31, 2020, Atlas had an unencumbered asset base including 31 vessels with a book value of $1.1 billion.

Valuation

So what is the company worth? Atlas would fit the Peter Lynch archetype of a slow grower though it does have some characteristics of a cyclical. Though the return on invested capital is in the low single digits, the company has grown revenue from $565M in 2011 to $1.4B in 2020 - just under 10% CAGR despite a near meltdown in the global shipping industry in 2016-17 due to the Hanjin Bankrupcty wiping out 98% of $10.5B in debt.

My method of evaluating a business begins with Aesop-style simple math of a discounted cash flow analysis on normalized earnings to attempt to assess what the current market price implies about the future. Taking 2017 - 2019, the average EPS would be $1.311.

Base case assuming 2% earnings growth from $1.31, a discount rate of 15%, and a 15 terminal multiple in 2029, the present value of cash flows is $13.72 which is near the current price. Increasing that earnings growth to 8% gives a present value north of $25, and a unlikely 15% gives us $40.

Analysts believe 2021 EPS will be in the $1.20 - $1.56 range and a similar range for FY 2022. It appears estimates will have a high probability of needing to be revised upward given the continual acquisition of new builds with charters in place, along with the potential for APR to contribute meaningfully.

As of March 8, 2021, 246.8 million common shares were outstanding, excluding 6.3 million shares reserved for future issuance to the sellers of APR per the terms and conditions of the APR acquisition agreement. Including that dilution, we reach 253.1 million shares. This places diluted revenue per share at $5.5, down almost 1/2 from the high in 2012. Dilution is certainly something to watch if revenue growth does not continue at very high rates.

Revenue increased to 25.6% to $1.421B in 2020 from $1.131

Shareholders’ equity has increased from $1.183 Billion to $3.625B in 2020.

Recently released FY 2021 low-end guidance for $1.325 billion from Seaspan and $180 Million from APR for $1.505 billion, an increase of 5.9%.

Purchasing ATCO here appears close to fair value, though a fifty-cent dividend makes it an easy pill to swallow. For a company that continues to trade below book value, along with EV / EBIT & Price / Sales ratios both below 5, it seems difficult to forecast a future where Atlas is not worth significantly more.

Granted, this is not a very precise look at the companies earnings power given the variation in cap-ex needed for long-term strategic operations. For an asset-heavy company like ATCO earnings per share tend to say less about the company than other metrics such as FCF. I’m choosing to use ‘17 - 19’ numbers as 2020 included quite a bit of cap-ex/writedowns that I don’t feel reflect a normal earnings year

Great article on a smaller cap company. Long $ATCO