Comerica Bank

“Comerica, originally called Detroit Savings Fund Institute, opened its doors on August 17, 1849, to a city bustling with shipyards, river trade, sawmills, horse-drawn carriages and dirt roads. It had six customers that day, with receipts totaling $41. Within two years, the patronage increased to more than 300 with the tally at $25,000.” - Comerica Investor Relations - Company History

The bank run seemed to be over, and the day after the Fed raised it was on again. Comerica is a bank that has been in the crosshairs and consistently shows up on all the lists floating around the internet. I’ve long been a shareholder, and have attempted to understand why it’s been driven so low, and that attempt thus far has failed.

Valuation

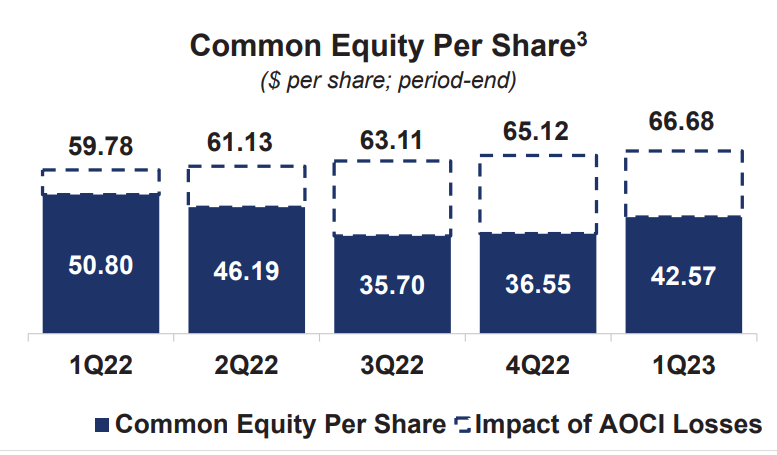

Comerica has a book value of $42.57, down from nearly $60 a share a year ago. This assumes a lot of things have to continue to go wrong, deposits have to continue to flee the bank, and losses have to mount. All of these things seem low probability.

Management

The CEO has been a banker for 37 years, 14 with Comerica. He makes north of $8M a year to run the bank; 88% of his salary is a bonus, and he has $40M in stock. Skin in the game. He did get one of the largest raises in the industry last year, but the bank has been doing well. The rest of the management team is over-paid, tenured, and stable.

Performance

The bank’s return on equity for the most recent quarter was 24%. (JPM was 18%) Net loan charge-offs were -.01%. This level is one of the lowest in the industry and an ROE higher than nearly every large bank in North America. Comerica had a strong net interest income of $708M in the first quarter vs. $456M in 1Q22. Interest rate increases have benefited Comerica, which has an incredible sub .5 efficiency ratio Commercial Bank, an average Retail bank, and a slightly above Average Wealth Management division (Average ROAs: 1.71%,-.14%, 1.21% respectively). The average rate on the loan book is 5.45%, generating $719M last quarter. This increased to 5.89% this quarter, and $777M. It will be even higher the rest of the year due to rate increases.

Financial Position

Deposit balances have left the bank, from $71.4B to $64.7B as of March 31st. Far from the run seen from at SVB and FRC. 54% of deposits are within the Commercial Bank, and 37% are within the Retail. It’s unlikely commercial lenders who have large balances are going to pull their money out when their average relationship is >15 years. 53% of the bank’s deposits don’t even pay interest. Total liquidity is 42B, which includes borrowing from the Fed’s discount window.

FHLB

“At March 31, 2023, investment securities with a carrying value of $18.1 billion were pledged where permitted or required by law. Pledges included $9.7 billion to the Federal Reserve Bank (FRB) for potential future borrowings” - 2023 10-Q Q1

Comerica has accessed the Fed’s Bank Term Lending Program, which in short makes the likelihood they will need to liquidate their assets very slim. $18.1B of their $18.295B of market value investment securities are pledged to this program, which allows the securities to be utilized as collateral for liquidity needs.

Securities

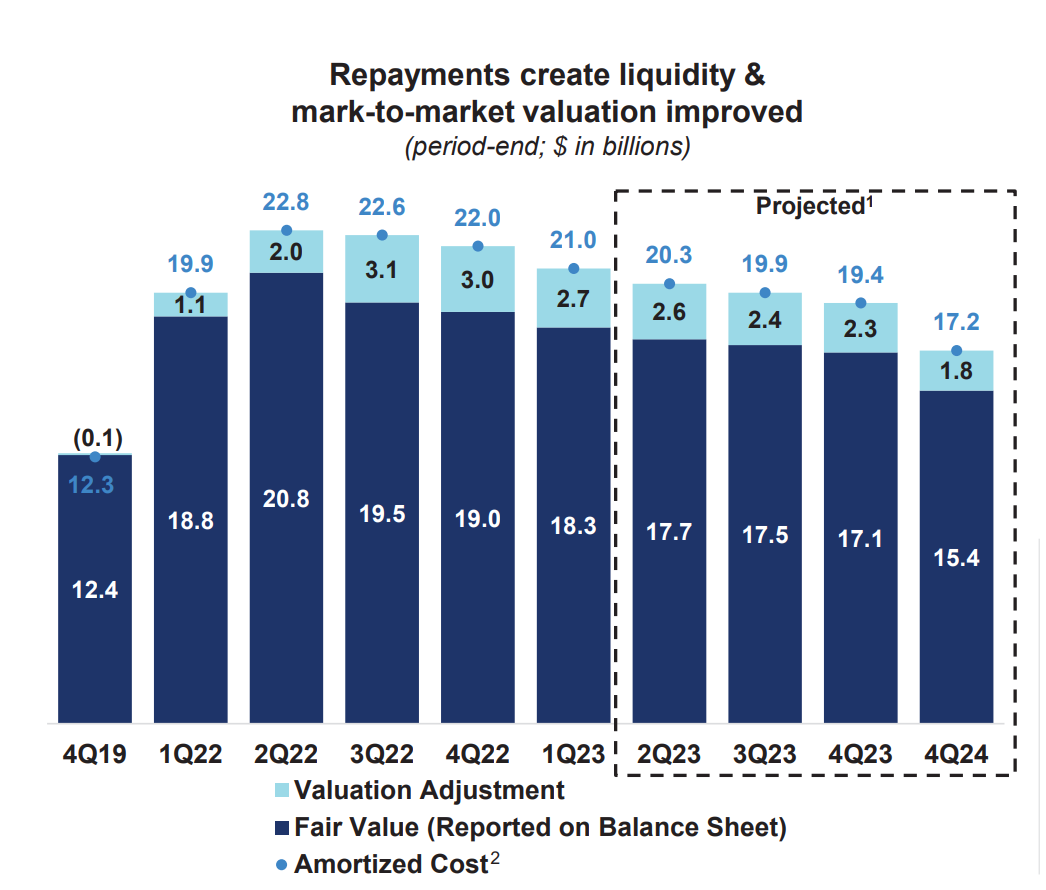

The securities portfolio is being run off, providing $20.3B in liquidity in the next quarter. All the bank needs to do is survive, and the mark-to-market losses will never materialize. Comerica did the smart thing and pledged 100% of its portfolio as available for sale, meaning the balance sheet reflects reality and unamortized losses are passed through the equity statement in the form of AOCI. In short, these losses will turn into gains.

Comerica is trading for its equity value and the market is assuming that all of the losses in AOCI are materialized. Every quarter that Comerica survives, that becomes a false prophecy.

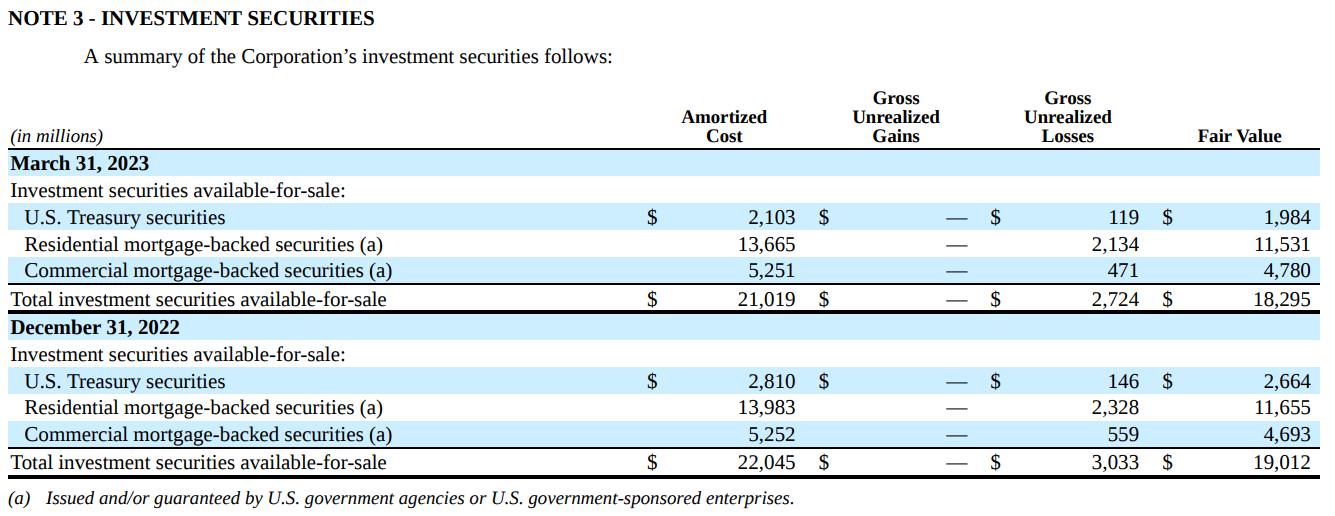

Looking at Note 3 from the latest 10Q is the most critical piece of information. Comerica had $3.033B in gross unrealized losses on Dec 31. 2022. Just 3 months later, that number was $2.724B. Substantially all of this came from commercial and residential mortgage-backed securities.

“Further, the Corporation does not intend to sell the investments, and it is not more-likely-than-not that it will be required to sell the investments before recovery of amortized costs. At March 31, 2023, the Corporation had 1,269 securities in an unrealized loss position with no allowance for credit losses, comprised of 23 U.S. Treasury securities, 993 residential mortgage-backed securities and 253 commercial mortgage-backed securities” - 2023 10-Q Q1

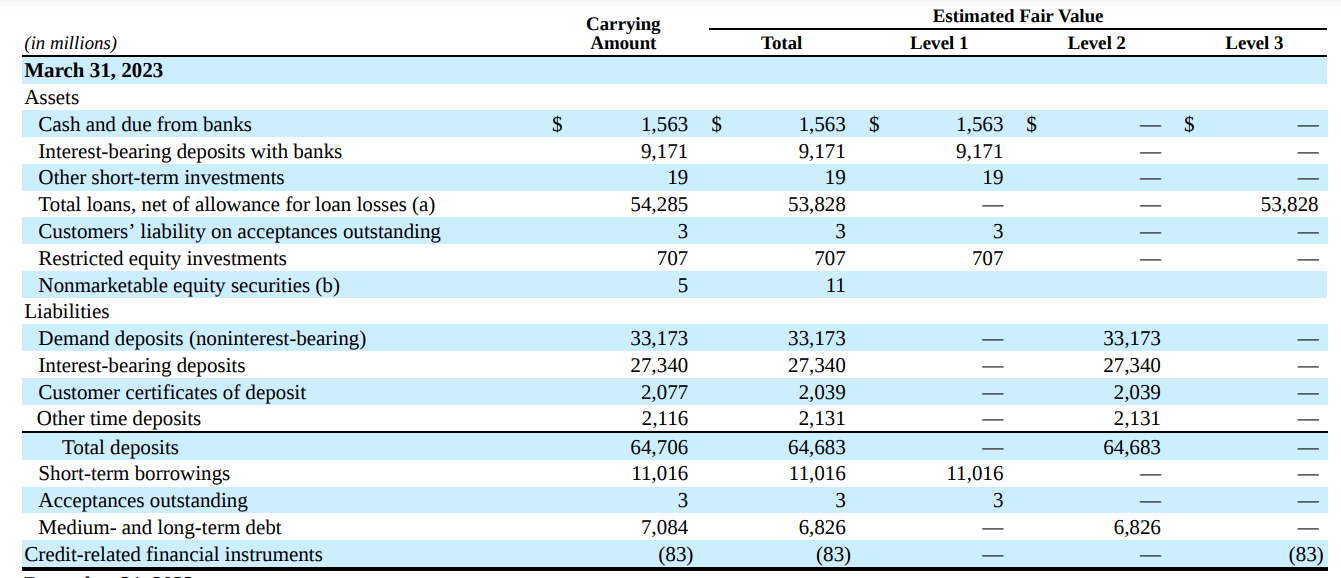

Other good signs are medium and long-term debt has appreciated from $6.82B to 7.08B

In closing - Shareholder’s equity actually increased to $5.7B 1Q2023, nearly $500M more than last quarter. Despite deposits declining, I want to own a business that’s increasing in value this much.

Disclosure - I added 100 shares to my long position today.