Comerica - Pounding the table $CMA

Comerica - Pounding the table $CMA

Additional 8K Reveals healthy business

Comerica Bank (NYSE: CMA) released an 8K a few weeks ago. It’s become my largest holding by far, and the story remains the same. Below I’ll discuss some elements from the most recent 10Q and explain why I continue to look at this bank as a misunderstood story that requires an accounting lens. I remain perplexed and wonder what I am missing. My basic thesis continues to be highlighted by the bank:

Ex-AOCI Common Equity should be accepted as the reality (currently $68 a share up from $61), as the losses in the securities book are unlikely to materialize absent a meltdown in the MBS market.

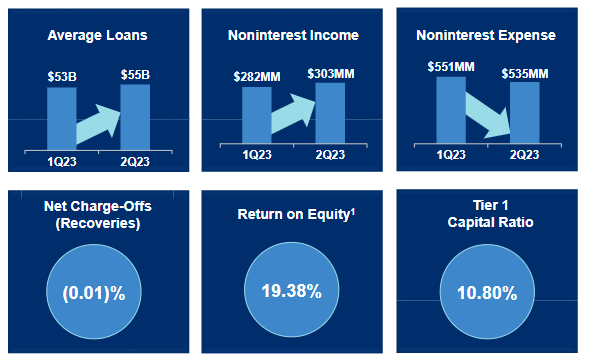

Not only is the loan book continuing to increase, but the charge-offs are non-existent. The bank is very good a lending money.

Liquidity will remain ample, and sufficient

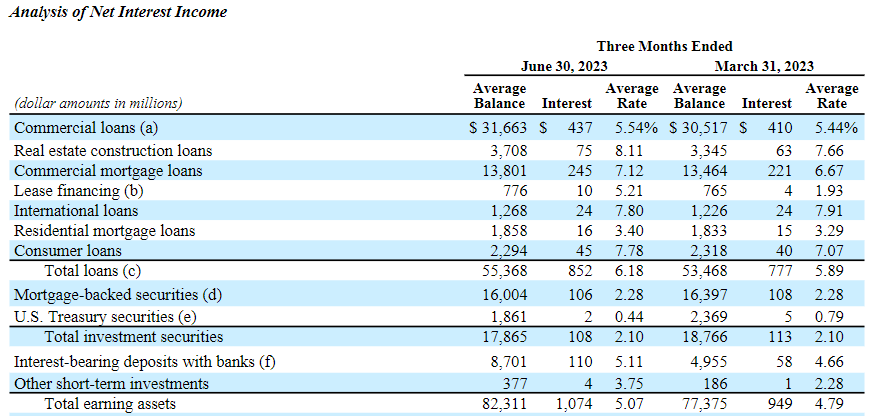

$1.861B in Treasures, down from $2.369B in the first quarter is a huge drop of over $500M. Given that they are only paying .44% this is to be expected in the current interest rate environment. The key takeaway is that much of the investment securities are not being sold, they are being redeemed at par.

The company's large unrealized losses of $2.6 billion in mortgage-backed securities (MBS) are the primary reason why its stock is where it is today. In the same quarter of 2022, the company's unrealized losses in MBS were only $1.1 billion. This significant increase in unrealized losses is likely due to the recent rise in interest rates, which has caused the value of MBS to decline.

It is important to note that unrealized losses are not actual losses until the securities are sold. However, even unrealized losses can have a negative impact on a company's financial performance. In addition, unrealized losses can also (and have) lead to credit rating downgrades, which can increase the cost of borrowing.

Despite the recent increase in unrealized losses, there are some positive signs in the company's MBS portfolio. The company's MBS balances improved by $100 million this quarter, from $2.7 billion to $2.6 billion. Improvement in its MBS balances is a positive sign. All in all, roughly $600M in unrealized losses rolled off this quarter.

CET1 ratio is ~10% (Regulatory minimum is 7%), NII above at $621M, robust fee generation, and a solid efficiency ratio of 57.7%. JPM has an efficiency ratio of 59%, and BOA sports 53%.

Net Securites-related AOCI decreased to $2.1B and is expected to decline another 32% by 2024. Commercial loans continue to be a big part of the story, with healthy growth in the California and Texas markets, 70% of which have recourse.

Under the BTFP (2.0 version of TALF from 2008 essentially), eligible depository institutions can borrow up to one year in length at a fixed interest rate of 0.50%. The loans are collateralized by U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets.

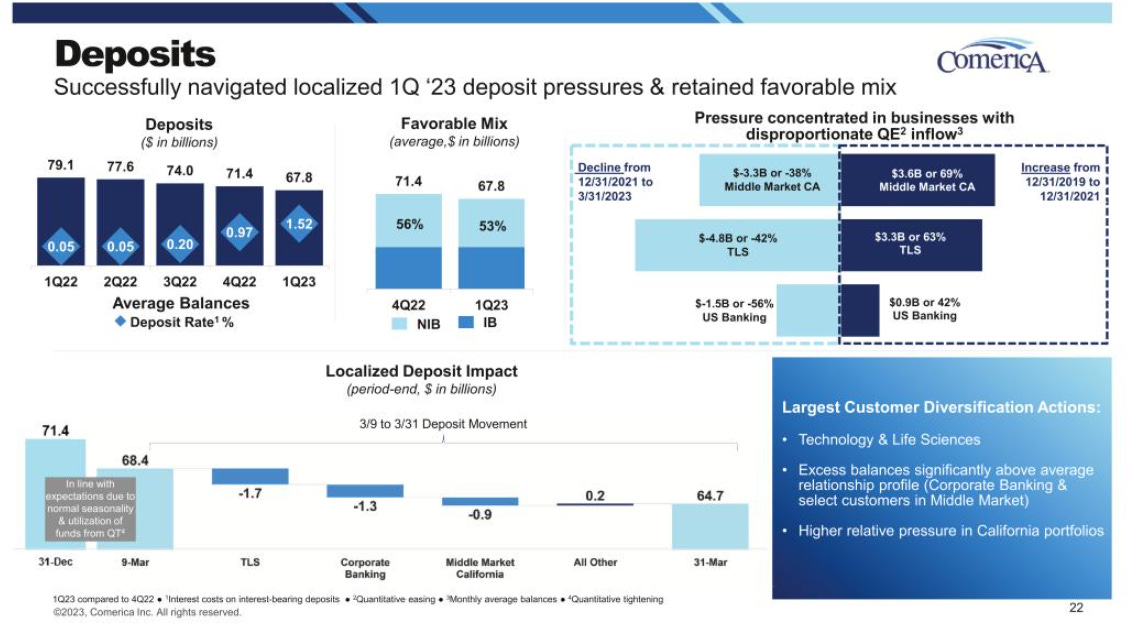

As of June 30, 2023, Comerica pledged loans totaling $25.0 billion and investment securities totaling $8.9 billion to the FRB lending program, which provided for up to $20.3 billion and $10.8 billion of collateralized borrowing through the discount window and BTFP program, respectively. Total available collateralized borrowings with the FRB totaled $31.1 billion on June 30, 2023. Given the total decline in deposits from $79.1B to $67.8B, I think it’s unlikely Comerica will need this remaining capacity. Average loans increased $195 million, while average deposits decreased $2.4 billion last quarter.

$3.756B is sitting in Accumulated other comprehensive loss (AOCI). If it all comes out, as I continue to believe it will, 80% of the book value gets us to 54$ stock price. The company has missed earnings once in the last 10 quarters and beat the last 5 straight. The average price target from analysts is $52. I’m happy to collect the 7% dividend, accumulate shares, and wait.