Eurobank Ergasias SA (EGFEY ADR)

Eurobank Ergasias SA (EGFEY ADR)

Buy at the bottom

TDLR: Profitability continues to increase, all franchises producing high levels of RoTBV. Operating expenses stable. Asset quality dramatically improving. Real GDP growth in Greece is expected at 3.5% and 3.1% for 2022 and 2023, though likely to be revised down.

As recently as 2019, the best performing stock market in the world was located in Greece. Greece has been cheap for a while given significant austerity and remains that way today. Looking at the Global X MSCI Greece ETF (GREK) the Price/Book & Price/Sales ratios both remain below 1 (0.69, 0.76). Italy and Spanish indexes both trade above book value. One of the difficulties in investing in Greece is the asset quality, as we’ll see within our company below the main driver of change was repairing the asset side of the balance sheet.

The Eurobank Group is a financial organization that operates in Greece, Cyprus, Luxembourg, Serbia, Bulgaria and UK. It is the second-largest holding in the MSCI Greece ETF, and one of the four systemic Greek banks, the others being National Bank, Piraeus Bank, and Alpha Bank.

Eurobank was named Best Consumer Digital Bank in Greece for 2020 by the internationally renowned American magazine Global Finance. Eurobank has additional operations in Bulgaria, Cyprus, Serbia, and Luxembourg.

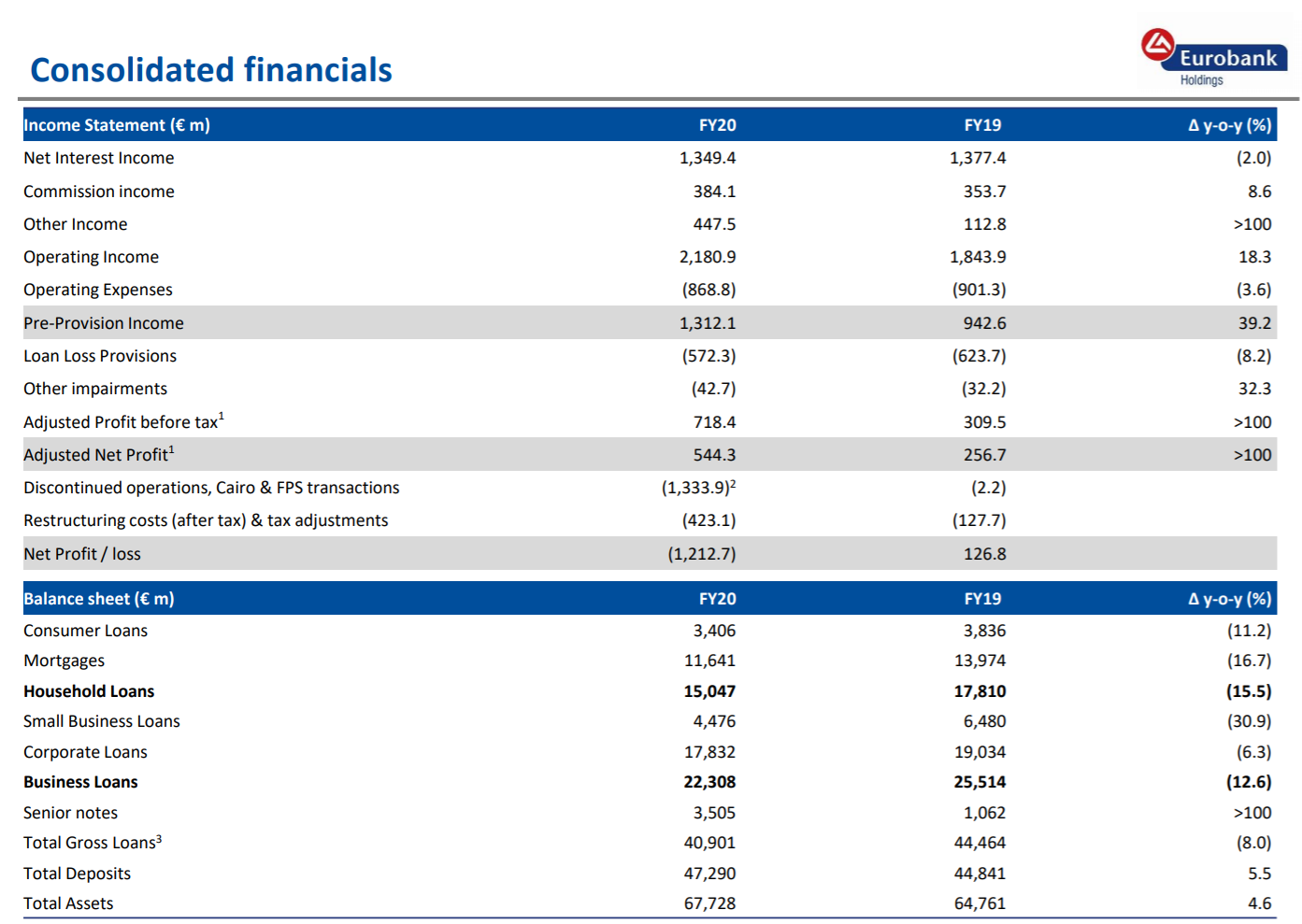

For a few years, things have been headed in the right direction for Eurobank. Operating income has grown, and non-performing entities (NPEs) have declined through massive securitization schemes (code-named Cairo, and recently, Mexico) designed to remove them from the balance sheets to separate entities (‘bad banks’) in a ‘hive down’ procedure. 2020 hit Greece particularly hard, with real GDP at -8.2% (better than expected -10% forecast from the European Comission1) after 1.9% growth in 2019.

While loan growth slowed dramatically in FY20, assets and deposits continued to increase. GDP growth has returned to positive territory (4Q20 2.7% q-o-q) and real estate prices have continued to increase. Real estate is a point of major concern for Eurobank because they acquired Grivalia Properties REIC in 2018 for €780.

This deal was brought to one of the main architects of Eurobanks’ recovery, and the reason why it came across my radar in Prem Watsa of Fairfax Financial Holdings. Prem is also the majority shareholder in Atlas, another of my interests. Fairfax owns 31% of Eurobank at a carrying value of $1.03 per share, which exceeds the current market value providing them with a slight deficit to the current share price. Fairfax has been investing money in Greece since 2010 and mostly losing, but it does appear that this is about to change.

Eurobank posted €305 in profit in 1Q22, on pace for the goal of €610m for FY22. Non Performing Entities (Loans from banks (mortgages, funding, loans) that debtors are no longer able to repay regularly totally.) have been steadily declining since FY2016. As of 1Q22, the Tangible book value is now €1.45.

The Winter 2021 Economic Forecast projects that the euro area economy will grow by 3.8% in both 2021 and 2022.