Rave Restaurant Group

Rave Restaurant Group

Pizza Franchiser with an appetite for it's own stock

“You have to turn over a lot of rocks to find those little anomalies. You have to find the companies that are off the map - way off the map. You may find local companies that have nothing wrong with them at all. A company that I found, Western Insurance Securities, was trading for $3/share when it was earning $20/share! I tried to buy up as much of it as possible. No one will tell you about these businesses. You have to find them.” - Warren Buffett

Rave Restaurant Group, Inc. owns and operates franchises, licenses, and supplies Pie Five and Pizza Inn restaurants operating domestically and internationally. The company has 3 segments, Pizza Inn Franchising, Pie Five Franchising, and Company-Owned Restaurants. It has 24 employees and a Market Cap of $23.8M. I don’t recall how I found out about it, but I’ve been watching it for a few quarters and finally decided to invest.

Rave has 275 Locations, Pizza Inn is one of the oldest brands in Dallas, as the first Pizza Inn opened in 1958. Pizza Inn and Pie Five are the two distinct brands, the latter launched in June 2011. Rave is focused on Pizza Inn Buffett's development in the Middle East in particular, as well as franchised Pie Five units domestically and internationally.

At first glance, the franchise fees for a Pizza Inn are on the lower end for a sit-down restaurant that seats over 50 people. A Subway franchise fee is $10-15k. A taco bell is $45k. Rave’s fees seem pretty standard.

Last year, Rave repurchased 493,474 shares for $1.04 and had the authorization to purchase $8.016M shares with no expiration.

Pizza Inn sales increased 24% from FY21 to FY22, and Pie Five increased by 17%.

Net income for 2022 was $0.45 a share. Where things get interesting are the revenue numbers. Revenue for FY2022 was $10.7M, and net income was $8M. Pretty good margins for a Pizza place. The reason being as of June 26, 2022, the Company had net operating loss carryforwards totaling $23.1 million that are available to reduce future taxable income and will begin to expire in 2032, of which $1.8 million are limited to 80% and do not expire. This allowed for a $5.657M tax benefit, which raised EBIT from an 11% increase over FY21 to a 5x.

Rave actually had a net decrease of 7 units due to various factors, many COVID related. The company actually closed its single remaining company-owned Pie Five restaurant in 3Q 2020. So now we are talking about an asset-light, franchise model.

Excluding the accounting minutiae there is still lots to like. $7.7M in cash underscores $10M in current assets and only $2.8M in current liabilities. The equity value of the company more than doubled in FY22 from $5.7M to $13.4M.

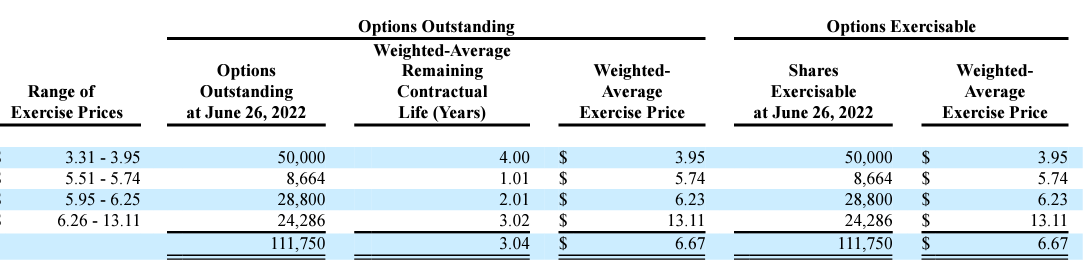

The options outstanding at $4 a share lead one to believe that there is an incentive to increase the stock price. During fiscal 2022, 493,474 shares were repurchased and, as of June 26, 2022, there were 354,951 shares available to be repurchased under the plan.

Running the show is Brandon L. Solano, who used to be the CMO of Pei Wei. He began his career at Domino’s Pizza as VP of Innovation and then spent 10 years as CMO of Wendy’s. Brandon has reduced debt, fully recognized the aforementioned tax benefit, and repurchased 1.1M of common stock. He has an MBA from Notre Dame and lives on a sustainable urban farm in Texas. Interesting fellow.

The latest quarter was another profitable one. The Company had a net income of $0.3 million for the three months ended March 26, 2023, compared to a net income of $0.5 million in the comparable period in the prior fiscal year, on revenues of $3.0 million for the three months ended March 26, 2023, compared to $2.6 million in the comparable period in the prior fiscal year. A 15% YOY increase. Net Income did decline, but it was mainly due to taxes.

Valuation

Taking the deferred tax asset out of the equation, earnings per share increased by 2.57% from FY 21-FY22. Not amazing growth and an implied multiple of ~16. Given that same multiple and growth discounted by 15%, which I would think appropriate for this level of risk, we arrive at .89 cents a share. That’s about a 60% downside from the current stock price - not a great margin of safety.

However, given the NOL carryforwards, taking the 45 cents earned last year, forecasting a perpetual sales decline of 5% yearly (at the same 15% discount rate) we arrive at $2.03.

My favorite scenario, with sales increasing 5% for ten years, gives us $3.66 (again, same 15% discount rate). The company eliminated long-term debt and is able to fund operations from cash on hand. It seems like a lot would have to go wrong for this business model which has potential in the right hands.