TripAdvisor ($TRIP)

Put a Fork in It.

Trip Advisor is the next Blackberry. It’s Dempster Mill Manufacturing Company - a dying business that will likely survive in another form. It’s a conglomerate with a discount attached. It’s Blue Chip Stamps with See’s Candies already a subsidiary.

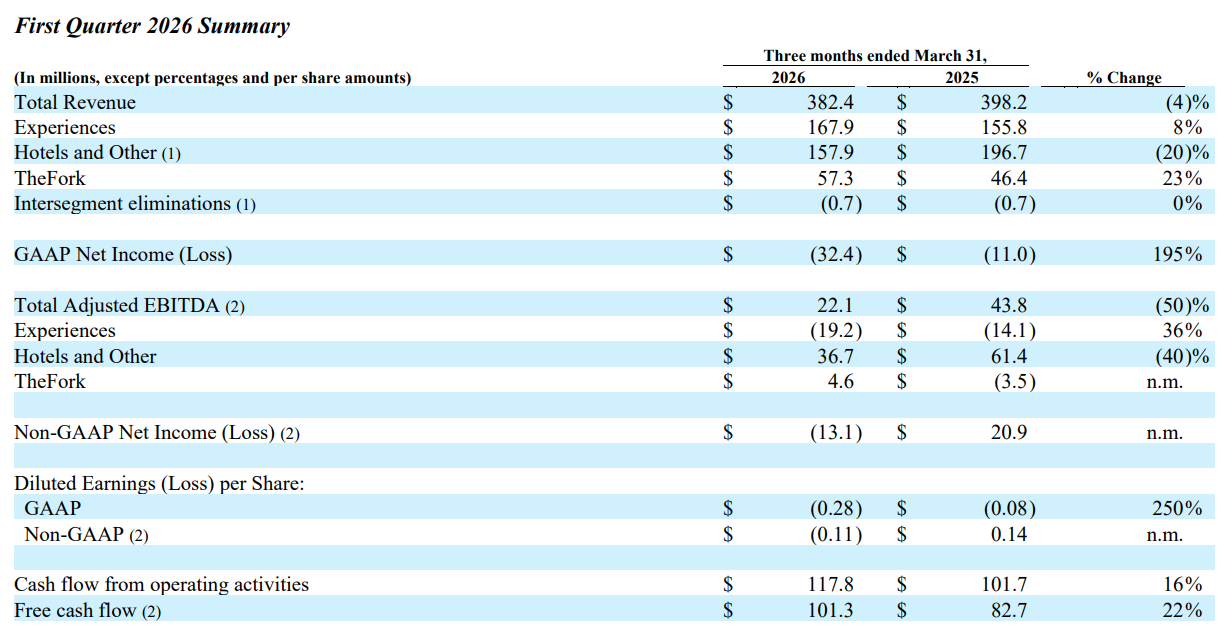

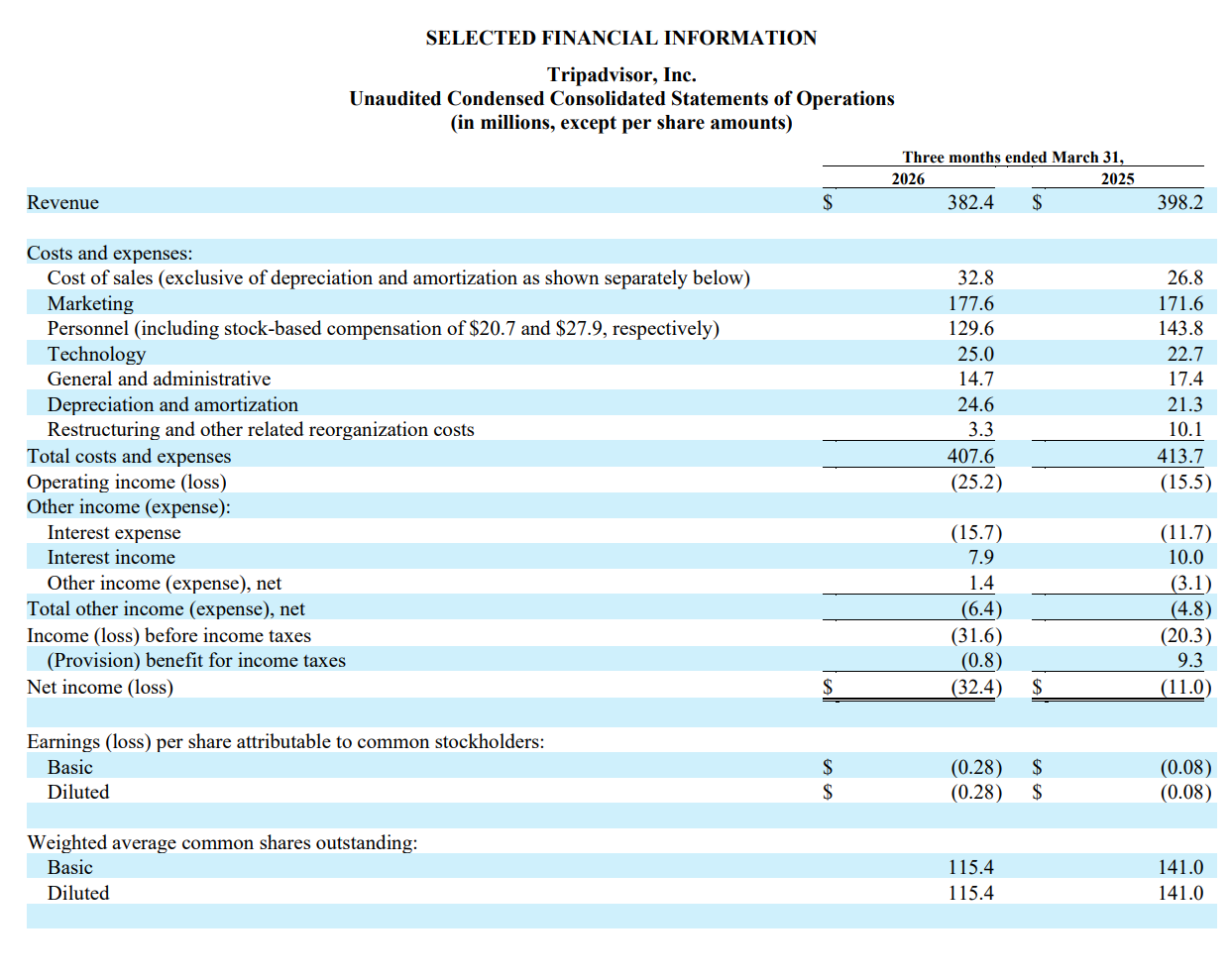

Trip reported 5.7.26 with mixed results. While Experiences grew, it’s not yet reached profitability. The legacy hotel website, and the source of the Dempster Mill analogy, continues to decline. Let’s assume it continues to decline at the same rate.

The 3-Year Projection (Revenue)

Using the current annualized revenue base of $631.6 million (based on Q1’s $157.9M), the trajectory looks like this:

Year 0 (Current): $631.6 Million

Year 1 (2027): $505.3 Million

Year 2 (2028): $404.2 Million

Year 3 (2029): $323.4 Million

Let’s assume that in ‘29, the margin continues to compress (as they did in Q1 from 32% to 23%) and settle at 15%, as this is still a software company. This would give us EBITDA of $48.5M. Slap a reasonable 5x on that, and this business is worth an estimated enterprise value of $242M. A stark contract from the $158M it just did in revenue in one quarter.

If we discount this back using the 30 year treasury rate to today, we arrive at $212.5M, for a worst case scenario. A best case would be the company figures out out to utilize this entirely unique data set in the AI era, and it’s worth double this if not more.

TheFork is another story. TheFork went from a Q1 2025 Adjusted EBITDA Margin: -7.5% (a loss of $3.5 million on $46.4 million revenue) to a Q1 2026 Adjusted EBITDA Margin: 8.0% (a profit of $4.6 million on $57.3 million revenue). That’s a 1,550 basis points (15.5%) year-over-year expansion.

While revenue grew by 23% ($10.9 million increase), total adjusted expenses only grew by approximately 6%. This suggests the platform is now successfully scaling its fixed costs (personnel and technology) against a larger booking volume. Booking volumes grew by 6% which is not mind blowing, but it’s growth.

If revenue growth (23%) continues to outpace booking growth (6%), it must mean higher revenue per booking. Could this be coming from the use of AI? Meta just reported their best quarter post-Covid. It seems this was the reason why for them.

It’s a guess what TheFork is worth - the OpenTable of Europe. For context, OpenTable was bought by Booking Holdings for 13.7x its 2013 revenue. Let’s slow TheFork growth down to far slower - to just inflation plus 3% - even though it’s grown quite a bit. TheFork has maintained an average annual revenue growth rate of 22.4% over the past three years.

While individual quarters have fluctuated between 12% and 28%, the full-year performance shows a consistent upward trajectory as it scales across Europe. Yet, let’s slow it down - and it still reaches $270M in revenue by 2029. Maybe this company isn’t anywhere near as dominant as OpenTable, so it’s only worth 5x it’s 2029 revenue. Now we arrive at what has Bank of America and Starboard Value so excited. A business worth a present value of ~$1.16 Billion. Close to the value of the entire company today.

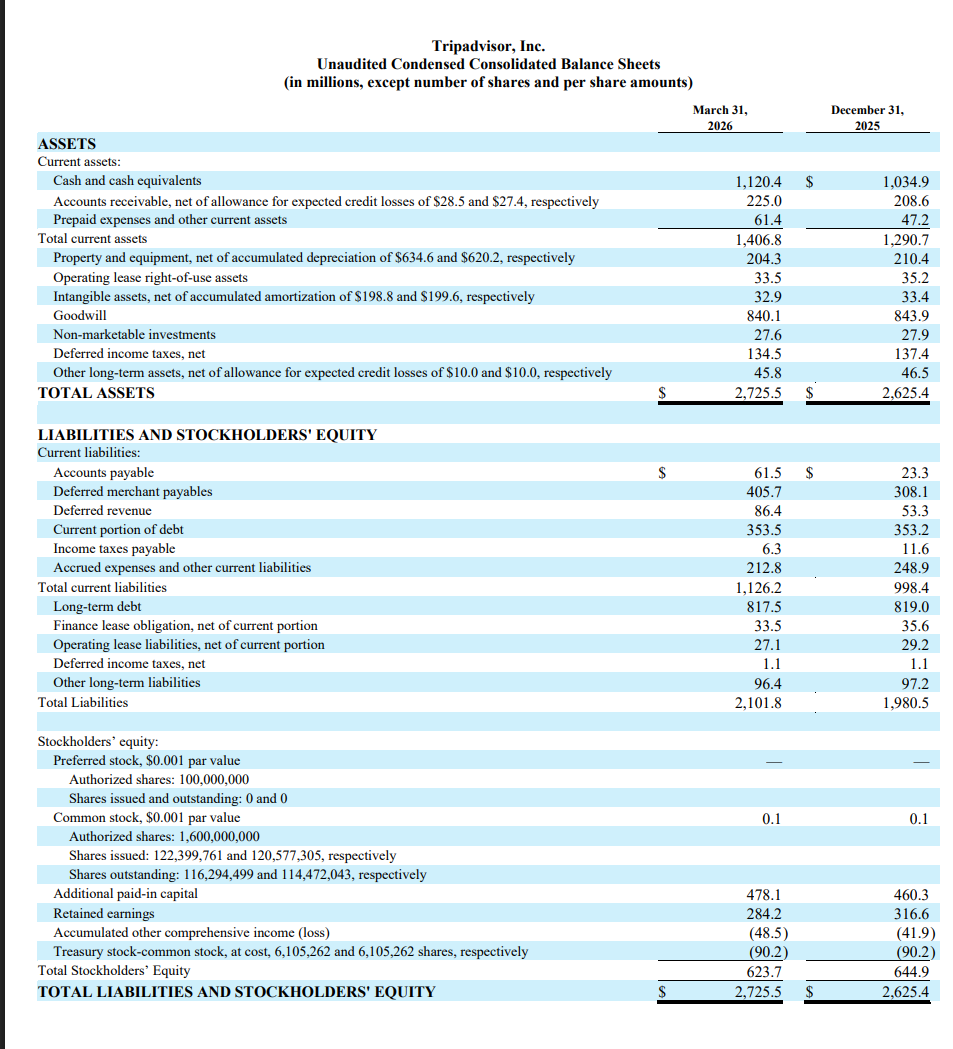

What about debt? TRIP reduced shares outstanding by 18.2% in one year, and paid back some debt, putting them at a net cash position of $775M against a term loan of $817.5 million due in 2030. With $100M in FCF a quarter, no problem there so I’m not factoring it in as it’s largely offset by the cash position.

Again, using the Buffet method of discounting via the treasury, with TheFork growing at ~22%, the Present Value of just this business line increases by roughly 17% every year you hold.

What about Viator, the European AirBNB for experiences, the 3rd business division that you get for free besides the ~200M legacy website? It’s revenue was $167.9 million (up 8% year-over-year) It’s not yet profitable, but management is targeting long-term margins of 20-25%. I’m not convinced of that yet since it’s not made money so far, so I’ll say this business grows at the same slow rate TheFork would (even though that’s far too conservative) at 3% plus inflation. Viator gets to $788.6 million in 2029 Revenue.

How much is it worth? Let’s assume it only reaches the average profit margin in the S&P 500 of ~11-12% and ~$90M in EBITDA. Using the same 5x EBITDA and discount method, Viator is a $392M business. A 5x EBITDA multiple is extremely low for a digital marketplace leader—typically, even “boring” companies trade at 8x–12x EBITDA in this frothy marketplace.

So Viator for $392M. Legacy website for $200M. TheFork for $1016M. We have a total equity value of $1,608M ($1.6 Billion) On 114 million shares this is a company trading below $12 a share, worth an extremely conservative $14.11 per share. BOA thinks it’s worth $2.5B, and Goldman Sachs thinks $22 a share. My my thoughts are at least 32% higher than where we are today.

I’m long just under 7,000 shares.