Comerica Q2 Earnings

Comerica Q2 Earnings

$2.01 in EPS. CET1 ratio 10.31. 57% Efficiency Ratio. 19.38% ROE

I’ve been a shareholder for some time but originally began writing about Comerica on May 4th, 2023, when I roughly tripled my position at $34. It has grown to be my largest holding through a spectacular run-up on the back of excellent results and a banking crisis that I believed was not going to affect the bank. Here’s an update on how it’s going.

Comerica reported a moderate beat in both revenue and earnings expectations for the 2nd quarter. The quarter was a mixed bag of results, but largely positive. Loan loss provisions continue to increase (increased $35 million to $728 million on June 30, 2023), however, net loan recoveries continue to exceed charge-offs.

Loans Increased by $1.9B

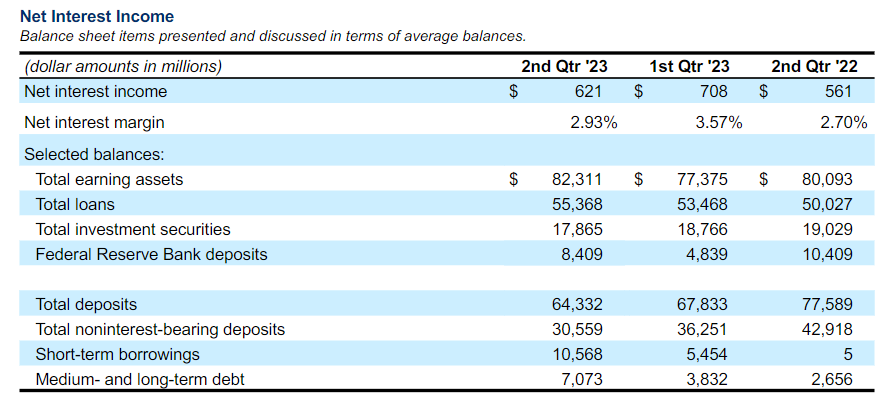

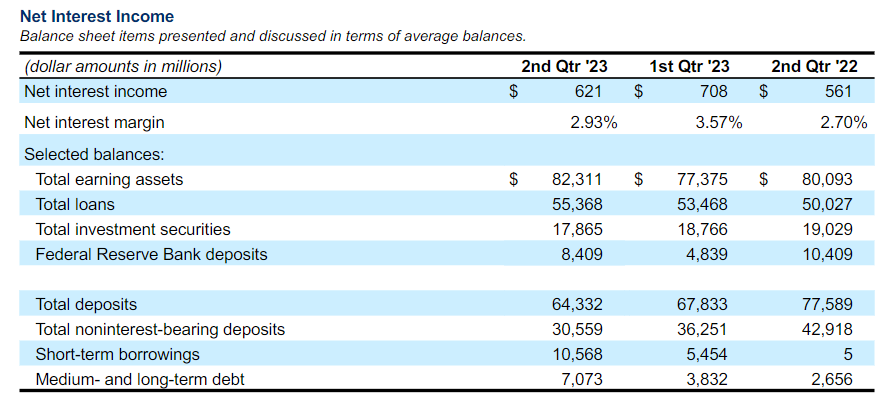

Net interest income decreased by $87 million to $621 million.

Deposits decreased by $3.5 billion to $64.3 billion

The average cost of interest-bearing deposits increased by 85 basis points to 237 basis points

Comerica’s strength remains within its excellent loan book and lending practices; nearly every segment continues to increase reaching $55.37B in total loans. Total assets have now crossed the $90B mark, and on the call, the CEO mentioned reaching the symbolic $100B mark organically which will likely bring more regulatory scrutiny.

Net interest margins were spoken about considerably on the earnings call, it’s expected that with increases in expenses in the back half of the year, as well as the continued increase in funding costs, the margin will settle a few basis points below the current level in the best case scenario. Zooming out to the YOY picture, NIM has increased to 3.24% over 2.44%, to $1.329B from $1.017B. A solid result.

While Interest income increased to $1.074B this quarter, total interest expense nearly doubled. Short & Medium term, as well as deposit costs, increased considerably. This was telegraphed and to be expected given the Federal Reserve’s actions. Guidance was given for this trend to continue. The interest expense increase is staggering, up $437M YOY, yet Comerica still increased net interest income even as the provision for credit losses tripled YOY.

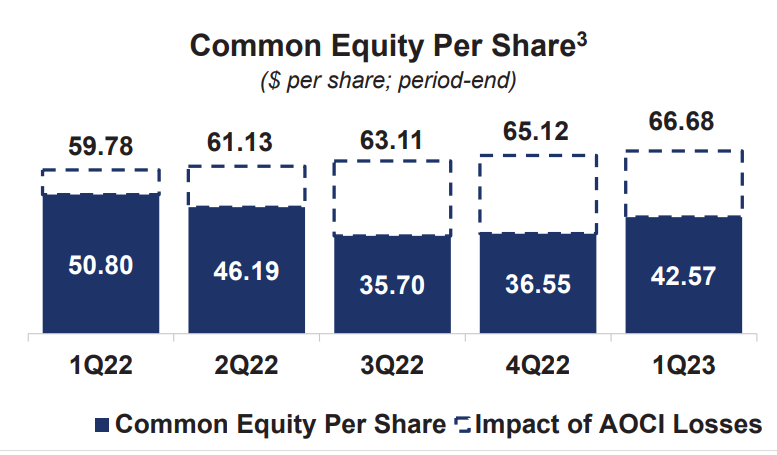

One point of concern is accumulated other comprehensive loss, which I’ve spoken about previously as a key metric. It increased this quarter driven by $585M in other comprehensive loss and gives the bank a $5.595B value in shareholders’ equity. This is a decline from ~$49 in GAAP book value to ~$42 as of June 30th, 2023. (On a Tangible level, $42 down to $39). This exceeds the previous guidance of $35.70 for this quarter.

Still, the thesis remains, if all of AOCI rolls off, and there is no forced selling of securities, book value continues to increase, reaching $8.314B, or $63 a share. The CFO confirmed on the call that there is no anticipated need for forced selling. Investment Securities Available - Held for sale decreased by $880M, so it seems the policy which was mentioned on the call to let these assets roll-off is intact.